Binance Wotd Words Answers Today [Solved] 25 April 2024

Binance Wotd Words Answers Today [Solved] 25 April 2024: CRYPTO WOTD Words Quiz Answers Today List New. Binance Wotd Words …

Binance Wotd Words Answers Today [Solved] 25 April 2024: CRYPTO WOTD Words Quiz Answers Today List New. Binance Wotd Words …

Binance WODL Answer Today 25th April 2024: Binance Word of the Day Answer, Binance Crypto WODL Answer Today, Today Binance …

Binance Word of the Day Answer Today 25 April 2024: Binance Word of the Day Answer, Binance Wodl, Today Binance …

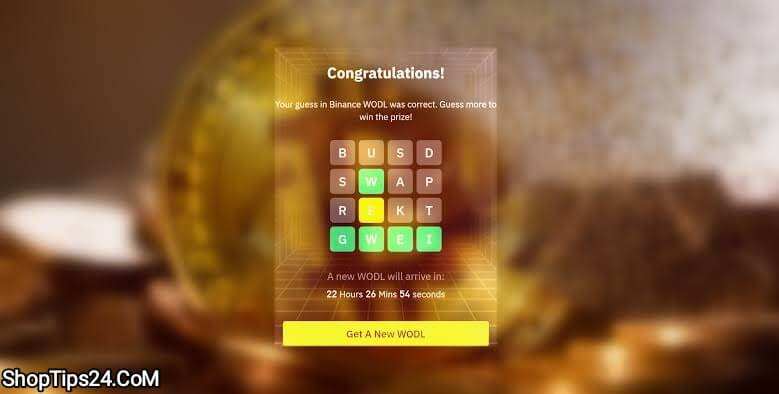

Binance WOTD Words 8 Letters Answers Today : Binance wotd answer today , Binance WOTD 8 letter words,Binance WOTD 8 …

Binance WODL Words 7 Letters Answers Today : Binance wotd answer today , Binance WOTD 7 letter words, Binance WOTD …

Binance WODL Words 6 Letters Answers Today: Binance WOTD Words 6 Letters Answers Today, Binance WOTD 6 letter words, Binance …

Binance WOTD Words 5 Letters Answers Today: WOTD Words 5 Letters Answers Today , Binance WODL 5 letter words, Binance …

Binance WOTD 4 letter words Today: Binance WOTD Words 4 Letters Answers Today. Binance wotd answer today , binance world …

Binance Wodl 3 letter words: Binance Wodl Words 3 Letters Answers Today. Binance wodl answer today , binance world answers, …

Binance Crypto Box Code – Earn Free Crypto Gifts Binance Crypto Box Code Free Reward Up to 10 USTD: 100% …